🔑 Sieva's favorite tweets this week + how to use your Roth IRA to invest

🔑#1 - Roth IRA for growth investments.

Roth IRA is an interesting investment tool.

When you contribute to your Roth IRA, you pay your current income tax rate. This is unlike 401k which is ‘pre-tax’.

Most CPAs will tell you that a Roth IRA is not a great idea. They recommend the 401k instead, here’s why:

- Contributing to your 401k reduces your gross income, so you pay less taxes today.

- Many people retire by age 60 which means you’ll be in a “low” tax bracket by the time you access your 401k.

- Investing in your 401k is ‘pre-tax’. This means you start with a larger investing base of dollars, which will likely grow faster than a smaller number.

- Roth IRA is particularly bad if you live in a high-income tax state like me (thank you California!).

However, I like to contribute to my Roth IRA every year, and I seek strategies that allow me to max it out. Why am I doing that?

I’m using this money to invest in high-growth investments (private companies, VC funds, or growth tech stocks). I use a self-directed IRA called Alto to accomplish this.

Here is the most extreme example of why this could be a good idea:

According to Silicon Valley lore, in the early days of Facebook, Peter Thiel made a $400k investment from his Roth IRA. Today this is worth Billions and it’s tax-free money.

If he had used his 401k, he would have had a massive income tax bill since in a 401k you pay your taxes on gains later.

I’m not saying any of us will ever be as lucky or good as Peter Thiel.

#2 - The Power of Leverage

It’s worth reading, and deeply understanding what Barrett here is talking about.

People born in the 80s and later are able to access incredible leverage like the world has never seen.

There are 4 categories of leverage:

- Labor

- Capital

- Code (Technology)

- Media (Audience)

When I started my first company, my margins were too low to only hire US labor. So I started offices in 3 different countries.

Without technology and labor as a tool, we would have never been able to grow our first business.

If you progress in your career, actively think of how you can apply each of these leverage points. Can you do your tasks 5 times faster, better, or cheaper using one of the strategies above?

🔑 What I’m reading this week

📫 Favorite Newsletter Tidbit in Psychology of Marketing

I love human psychology. Specifically, I get a kick out of behavioral irrationality.

We all like to believe we are “logical” beings. But the truth is: smart marketers are capable of controlling our decisions 🤓.

Check out the decoy effect written about here.

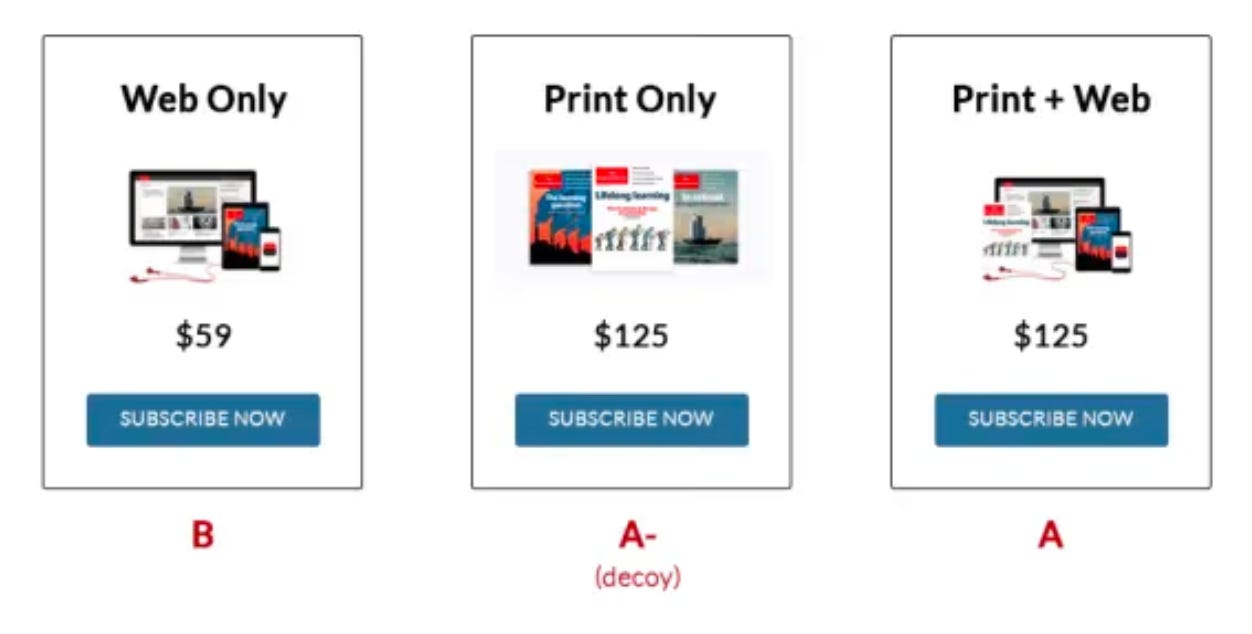

The Economist once ran a study. They offered 3 options:

Why would they offer the middle option? Seems silly right?

It’s a decoy.

They want buyers to spend more money. The decoy made people spend more money by picking the higher package more often.

When they removed the “decoy”, the number of people who bought the cheapest plan increased by 400%!!

📜 Book of the Week - The King of Oil. Marc Rich invented the spot/commodity market for oil trading. He brokered oil deals between Iran and Israel. He sold oil to Che in Cuba. He was marked as an enemy of the state to the US. It’s a thrilling read. Free if you use Libby app.

📫 Favorite Newsletter quote: Frameworks & Finance

When I talk to business owners, I always like to ask the question: how often do you look at your bank statement?

Too often, this answer is daily. Now, don’t get me wrong… cash balances are important…but the problem with this: it’s a lagging measure.

This quote from Kurtis Hanni perfectly summarized how I used to run my business.

I’d look at the cash in the bank account. If it was up, I was happy. If it was down, I was sad and would scramble to grow it.

The issue is cash in your bank is a lagging indicator. To manage your business properly you need to learn how to read a cash flow statement. You can read Kurtis’ advice on how to read a cash flow statement here (and you can signup for his newsletter too).

If you don’t understand all this immediately, remember what I said last week. Go easy on yourself. It will take a few dozen repetitions to start understanding it all :)

🔑 BONUS - Get My Free 100-Point Due Diligence Checklist

Last week, I sent you an offer to get a free copy of my 100-Point Due Diligence Checklist. 154 readers signed up to get it!

If want to:

- understand how we make business buying decisions, or

- you want to buy a business one day

Then this is a useful tool for you.

To access the Diligence List for FREE ⭐️invite 1 friend⭐️ to this newsletter (using this referral program).

You will immediately get a link to the Due Diligence Template.

👉 Join the referral program. You’ll get cool free gifts for referring your friends.

💡❓If I did a podcast interviewing small business owners about how they started the business and how they make money, would you listen?💡 Reply back to let me know.

I only want to interview owners of boring cash flowing businesses (not high flying tech companies).

Have a fantastic week,

~ Sieva